Smart card (integrated circuit card)

A smart card is a plastic card with an embedded integrated circuit used for secure identification, authentication, data storage and payment. It exists in contact and contactless forms and supports various applications.

A smart card is a portable card, typically made of plastic, that contains an embedded integrated circuit enabling secure storage and processing of data. The term covers both cards with contact pads and those that communicate wirelessly via an antenna. Smart cards are used to identify and authenticate users, to store credentials and small amounts of value, and to run simple applications directly on the card. For general reference see basic definition.

Image gallery

9 Images

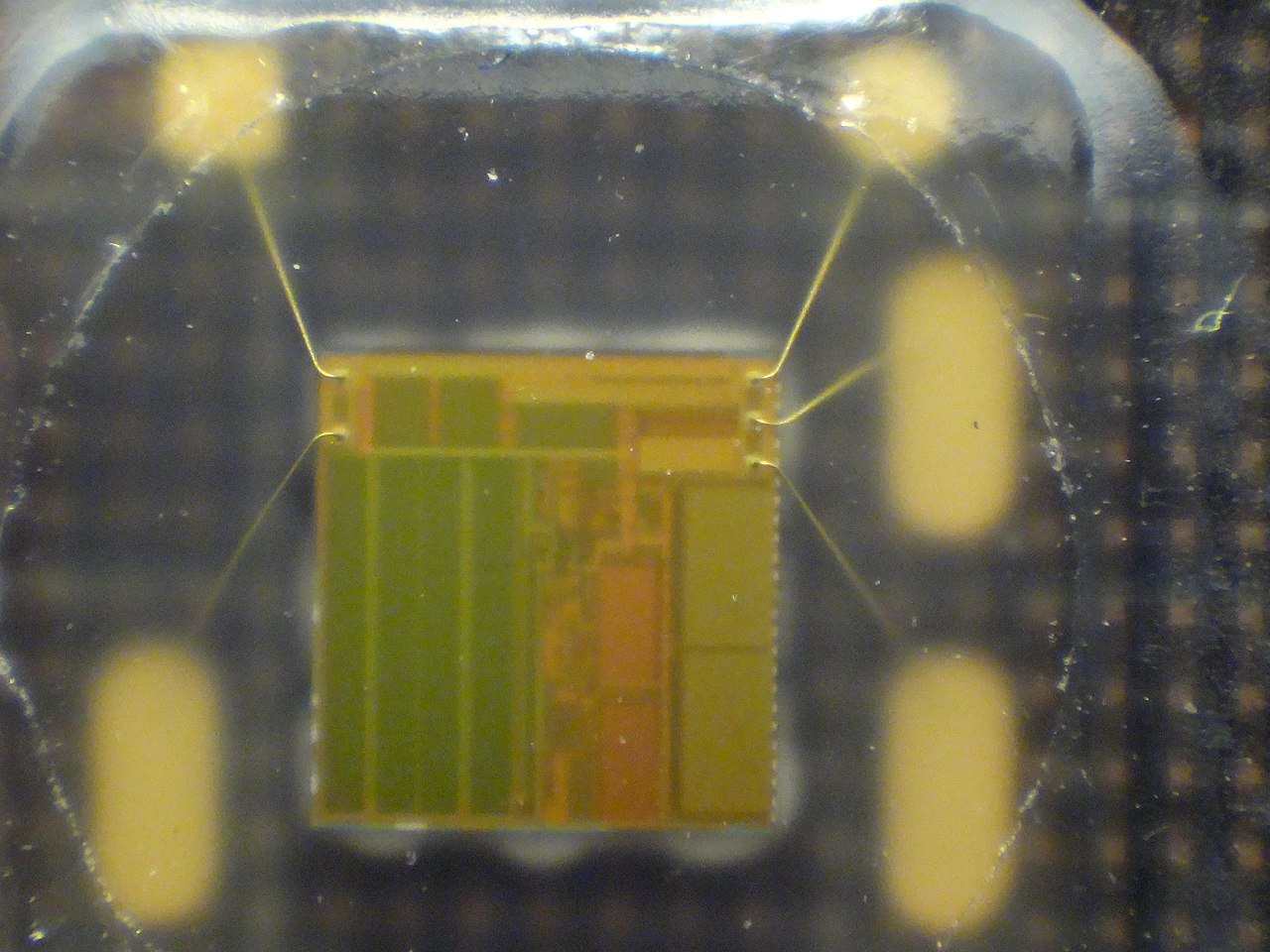

Characteristics and components

Internally a smart card may contain either a secure microcontroller (often called a CPU card) or only non-volatile memory (a memory card). Contact cards present metal pads on the surface to connect to a reader; contactless cards use an embedded antenna and radio interface. Many cards combine both modes as dual-interface cards. Smart cards can coexist with older magnetic-stripe systems: some payment and bank cards still include a magnetic stripe as a fallback magnetic stripe. Standards and interoperability are important; readers and middleware follow international standards for electrical, physical and communication characteristics (standards and authentication).

History and early use

Smart cards first reached wide consumer use in the early 1980s. One of the earliest large-scale deployments was in France, where payphone cards storing pre-paid credit were introduced to reduce coin use and support pay calls; the card reduced the stored balance as calls were made French payphone history and stored pre-paid credit. Alternative architectures have since appeared in which account balances are kept on remote servers rather than on the card itself; such solutions rely on network authentication and central databases remote balance systems.

Common uses and examples

Smart cards appear in many everyday applications. Bank and debit cards used at automated teller machines are often smart cards; they allow cash withdrawals after successful verification, sometimes alongside a magnetic stripe for compatibility with older terminals cash withdrawal and ATM. Cards commonly require personal identification numbers for user verification PINs. Smart cards are widely used for electronic payments and transport ticketing—examples include city and transit cards in Japan Japan, Singapore Singapore, and the Octopus card in Hong Kong Octopus Hong Kong—among many others payment systems.

Security and operation

Security is a principal attribute: smart cards can perform cryptographic functions, store keys, and enforce access policies inside the card's secure hardware. Authentication techniques include PIN entry, challenge–response protocols, and public-key operations. If a user enters the wrong PIN repeatedly many systems block the card to prevent fraud. Cards that hold monetary value may record transactions locally on the chip or interact with a backend system for authorization and settlement chip-based solutions.

Types, distinctions and notable facts

Common classifications include contact vs contactless, memory vs microcontroller, consumer vs subscription (for example SIM cards in mobile phones), and single-application vs multipurpose cards. Deployment scales vary from closed-loop systems—where a single operator issues and accepts a card—to open-loop payment networks accepted by many vendors. The choice between storing value on the card or in a central database affects privacy, offline capability and risk management. For technical details and standards, consult introductory resources and manufacturer documentation overview and standards.

- Contact card: connects via metal pads and physical reader contact.

- Contactless card: communicates by radio frequency and supports fast, tap-and-go use.

- Dual-interface: supports both contact and contactless readers for wider compatibility.

For further reading and implementation guides, see associated resources and technical specifications provided by vendors and standards bodies ATM reference, PIN practices, and case studies of transport cards Octopus case study.

Related articles

Author

AlegsaOnline.com Smart card (integrated circuit card) Leandro Alegsa

URL: https://en.alegsaonline.com/art/91194