1973–1975 recession

A widespread economic downturn in the 1970s marked by simultaneous high inflation and unemployment (stagflation), triggered by the 1973 oil shock and changes in the postwar monetary system.

Overview

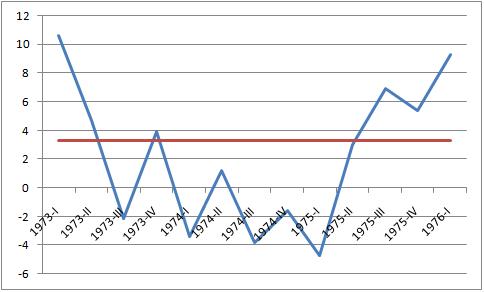

The 1973–1975 recession was a major downturn across much of the industrialized Western world that combined weak growth and rising prices. Unlike many previous postwar downturns, it produced sustained stagflation—a coexistence of falling output and high price increases—which challenged standard policy tools. Economists and policymakers described the period as one of pronounced economic stagnation interrupted by abrupt shocks and structural adjustments.

Image gallery

6 Images

Key characteristics

The episode was notable for two simultaneous problems: rising unemployment and persistent inflation. Labor markets deteriorated in many countries as demand weakened, while consumer prices accelerated because of supply constraints and monetary conditions. The combination of unemployment and inflation—each typically countered by different remedies—made policy responses difficult and often politically contentious. The phenomenon of rising prices amid weak output drew attention to new models of inflation that emphasized supply shocks and expectations.

Primary causes

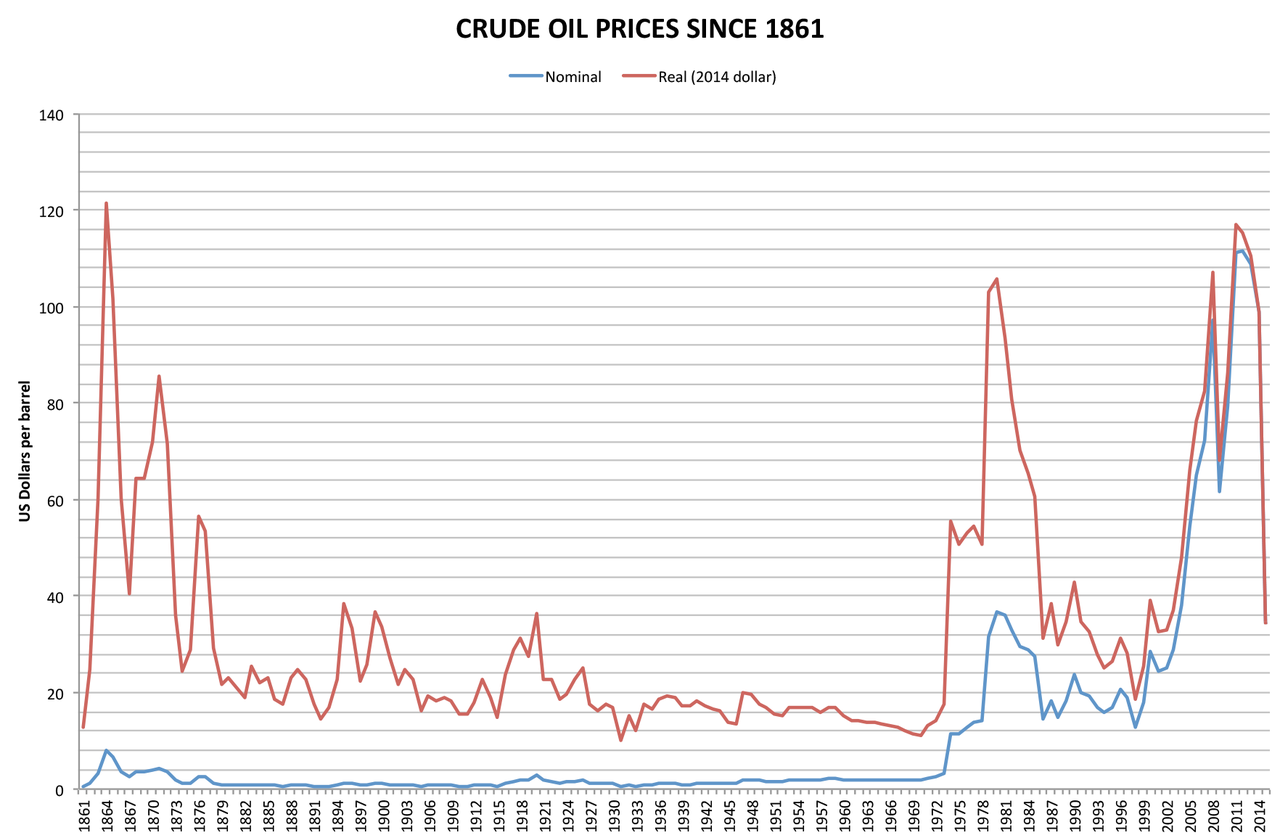

- Oil shock: The 1973 oil embargo and subsequent disruptions sharply increased energy costs and acted as a major supply shock to advanced economies, transmitted by higher production and transport costs (1973 oil crisis).

- Monetary and exchange-rate changes: The collapse of the Bretton Woods monetary order after the so-called Nixon Shock altered exchange-rate regimes and contributed to greater volatility and inflationary pressures (Bretton Woods).

- Structural and policy factors: Some economies were already facing productivity slowdowns, fiscal strains, and labor market rigidities that amplified the domestic impact of external shocks.

Timeline and national experiences

In the United States the official recession is dated from November 1973 to March 1975, spanning the later part of the Richard Nixon administration and into the presidencies of Gerald Ford and Jimmy Carter. The downturn and its inflationary aftermath influenced policy debates through the late 1970s and into the early years of Ronald Reagan's presidency. Other advanced economies experienced similar patterns, though timing and severity varied depending on exposure to energy imports, industrial structure, and domestic policy responses.

Policy responses and consequences

Governments and central banks used a range of tools—fiscal stimulus, monetary accommodation, income policies, and temporary price or wage controls—to try to limit output declines and tame price rises. Those responses had mixed success and sometimes prolonged inflationary expectations. The difficulty of managing simultaneous inflation and unemployment prompted a re-evaluation of macroeconomic policy frameworks and eventually led to tighter monetary policies in the late 1970s and early 1980s.

Legacy and notable facts

The 1973–1975 recession is often seen as a turning point in postwar economic history: it ended the era of stable low inflation and predictable growth and highlighted the role of energy markets and international monetary arrangements in domestic performance. It also stimulated research into inflation expectations, supply shocks, and the limits of demand-management policies. For further context on economic stagnation and policy debates of the period, see discussions labeled economic stagnation, stagflation, and the contemporary accounts of the 1973 oil crisis.

Related topics and primary-source materials are available via external collections and retrospectives that examine the political, social, and technical responses to the crisis; for entry points consult resources on the postwar monetary system (Bretton Woods), contemporary leaders (Nixon, Ford, Carter, Reagan), and analyses of unemployment (unemployment) and inflation (inflation).

Author

AlegsaOnline.com 1973–1975 recession Leandro Alegsa

URL: https://en.alegsaonline.com/art/133537