Disposable and discretionary income

Definitions and differences between disposable and discretionary income, how each is measured, their roles in household budgets and the economy, and limitations for policy and analysis.

Overview

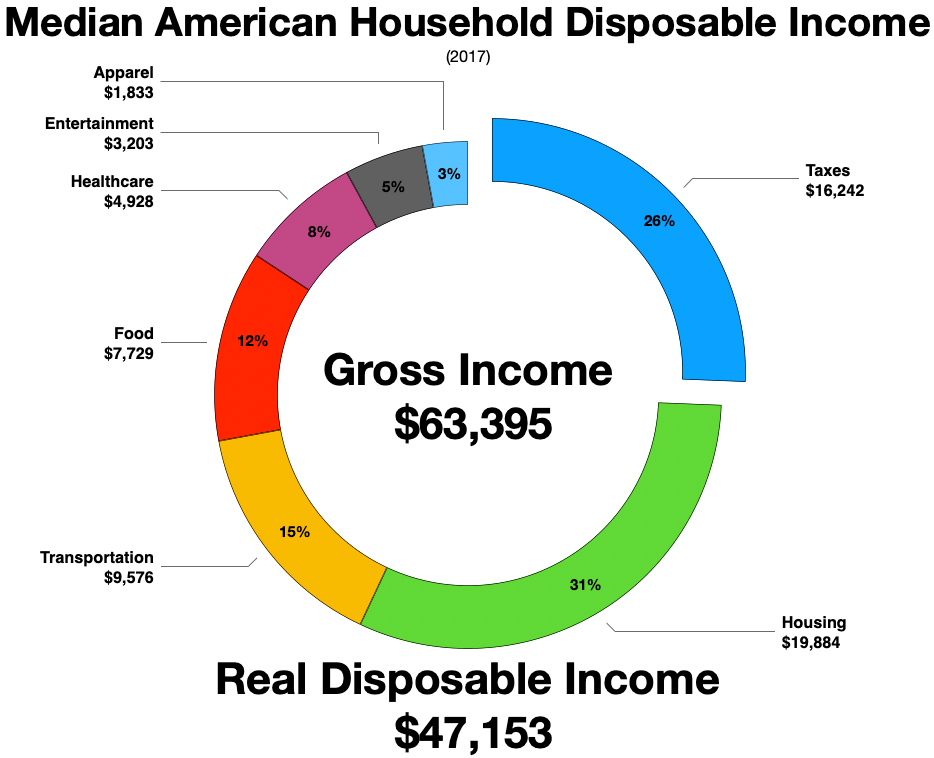

Disposable income is the portion of an individual's or household's earnings remaining after mandatory payments to government—principally income and payroll taxes. In national accounting this concept is often termed "disposable personal income" and equals total personal income minus current personal taxes. Discretionary income is related but distinct: it is what remains after paying for basic, recurring necessities such as housing, utilities, food and essential transportation.

Image gallery

3 Images

How it is measured

At a simple level, disposable income = gross personal income − personal current taxes. Economists and statisticians adjust this basic calculation in several ways, for example by including employer-paid benefits, social contributions, or by subtracting non-tax compulsory charges. Discretionary income is typically derived from disposable income by subtracting estimated essential living costs.

Characteristics and examples

- Disposable income: indicates immediate spending power for savings, debt repayment, or consumption after taxes. For formal definitions see an official definition.

- Discretionary income: suggests the share available for non-essential goods, leisure, luxury purchases, or extra savings once essentials are covered.

- Households with similar disposable incomes can have very different discretionary incomes depending on family size, housing costs, and local prices.

Economic and policy relevance

Disposable income is a key indicator used to assess living standards, save rates, and aggregate consumer spending. Discretionary income helps businesses forecast demand for non-essential goods and informs marketing and credit decisions. Policymakers monitor changes in disposable income to evaluate tax policy, welfare programs, and stimulus measures aimed at boosting consumption or relieving poverty.

Key distinctions and limitations

Differences between the two measures matter: disposable income is a broader accounting metric tied to taxation, while discretionary income is more subjective and depends on cost-of-living assumptions. Both measures have limitations—neither fully captures in-kind transfers, informal income, or sudden changes in expenses. Analysts therefore interpret these figures alongside other indicators to form a fuller picture of household financial health.

Related articles

Author

AlegsaOnline.com Disposable and discretionary income Leandro Alegsa

URL: https://en.alegsaonline.com/art/27710

Sources

- census.gov : "Archived copy"

- bls.gov : bls.gov