Microfinance: small-scale financial services for underserved people

Microfinance provides small loans, savings, insurance and payment services to people excluded from traditional banking, supporting livelihoods, entrepreneurship and financial inclusion with varied models and mixed outcomes.

Overview

Microfinance refers to a set of financial services offered to people who do not have access to conventional banking. These services typically include small loans, savings accounts, insurance, remittances and payment services delivered at low transaction sizes. Microfinance aims to broaden financial inclusion so low-income households, informal workers and small entrepreneurs can manage cash flow, invest in livelihoods and cope with shocks. Institutions that provide these services include non-governmental organizations, cooperatives, specialized microfinance institutions, and sometimes banks that operate dedicated programs. Traditional commercial banks often avoid very small accounts or loans because the administrative cost per client is high; microfinance providers use different delivery models to make small transactions viable.

Image gallery

10 Images

Services and typical features

Common elements of microfinance practice include:

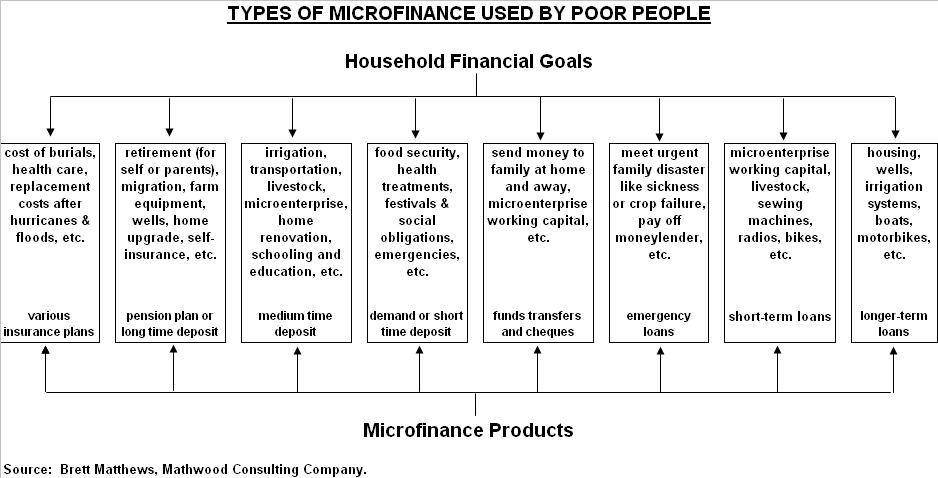

- Microcredit: small, short-term loans used for business start-up, working capital or household needs. Microcredit is often repaid in regular installments.

- Microsavings: deposits designed for irregular earners who need safe places to save and build buffers.

- Microinsurance: simple risk-pooling products that protect against health, crop, or funeral expenses.

- Payments and transfers: low-cost money transfer and payment services suited to informal economies.

Delivery relies on methods like social collateral, group lending and close staff-client relationships to reduce information asymmetry and enforce repayment without costly legal processes. Borrowers sometimes apply together in solidarity groups to share responsibility for loans; this collective approach substitutes for conventional collateral and is a distinguishing feature of many programs.

Models and institutions

Microfinance is implemented through a variety of organizational models. Examples include community-based savings and credit cooperatives, NGO-run credit programs, specialized regulated microfinance institutions, and commercial banks with targeted microfinance windows. Newer models combine digital payments and mobile banking to reach remote clients. Some platforms link small lenders and donors with borrowers, while others focus on sustainability and charging market-based interest to cover costs.

History and development

The modern microfinance movement grew in the late 20th century. Practical experiments with small loans for the poor preceded formal institutions; by the 1970s and 1980s several pioneering projects demonstrated that very small loans could be repaid. Since then the sector expanded globally, attracting public and private funding as well as debate about best practices and impact.

Uses, benefits and limitations

Microfinance can support income-generating activities, help households smooth consumption, and increase women’s access to financial resources in many contexts. Evidence about poverty reduction and long-term transformational impact is mixed: some borrowers use small loans successfully to grow businesses, while others struggle with irregular incomes or face over-indebtedness. Interest rates can be higher than conventional retail banking because of administrative costs, and regulatory oversight varies by country.

Notable distinctions and practical considerations

Microfinance differs from standard banking primarily in scale, client targeting and risk management methods. It emphasizes accessibility, convenience and non-traditional forms of collateral. When exploring or evaluating microfinance options, prospective clients and policymakers often consider affordability, transparency of terms, the reputation of the provider, and whether services are designed to meet long-term financial inclusion goals rather than short-term credit expansion. For more on how banks operate versus specialist microfinance approaches see banks, and for further reading about small loans see microloan resources.

Microfinance continues to evolve as technology, regulation and research shape how small financial services reach underserved communities.

Related articles

Author

AlegsaOnline.com Microfinance: small-scale financial services for underserved people Leandro Alegsa

URL: https://en.alegsaonline.com/art/64597