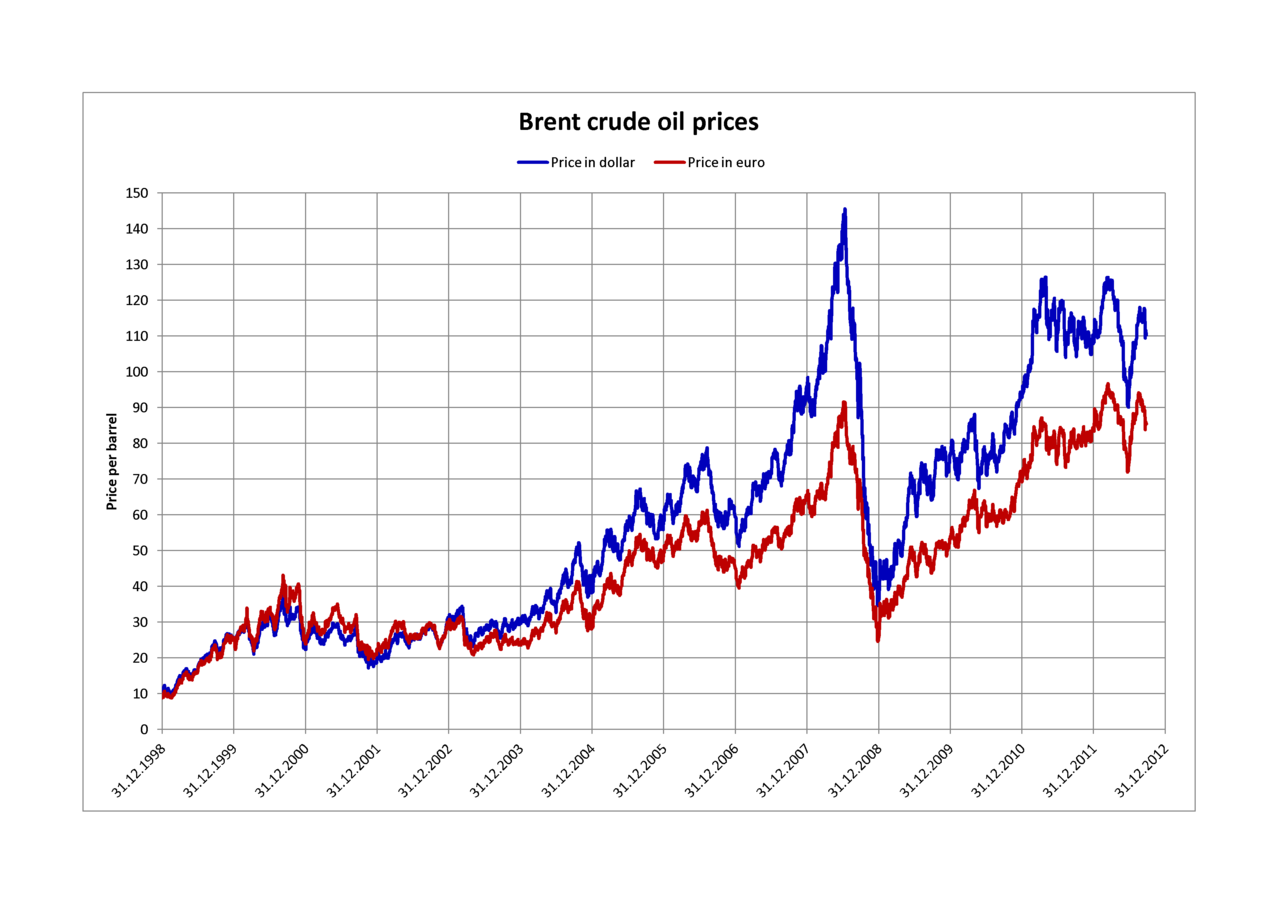

Brent Crude

Brent Crude is a widely used global benchmark for crude oil prices. Originating from North Sea production, it denotes a light, low‑sulphur blend used in trading, pricing and contract settlement worldwide.

Brent Crude is a primary international benchmark used to price large volumes of crude oil. The term originally referred to oil produced from the Brent field in the North Sea but has evolved to denote a blend of North Sea crude streams that underpin trading and settlement. As a trading classification it guides transactions across physical and financial markets: see general trading classifications via trading classification, and note the product itself is a form of crude oil. Brent is often paired with West Texas Intermediate for comparisons in market reports (WTI).

Image gallery

6 Images

Characteristics

Brent is described as "light" and "sweet": light because it has relatively low density and yields a high proportion of valuable light products such as gasoline and diesel; sweet because it contains comparatively low sulphur, which reduces refining complexity and emissions control costs. These qualities make Brent desirable for many refineries and an influential reference point for global pricing.

History and development

The benchmark traces its name to North Sea production and to market practices that developed as seaborne oil trade expanded. Over time the original single‑field product became represented by a managed blend and by different market instruments—physical daysales and dated cargoes, as well as standardized futures and swaps. Market infrastructure, such as futures exchanges and clearing houses, helped Brent become a dominant price signal beyond the North Sea region.

Market role and contracts

Brent prices serve multiple functions: they are a reference for long‑term contracts, a basis for spot cargo valuation, and a settlement mechanism for derivatives. Distinct contract forms coexist—physical benchmarks (sometimes called dated or cash Brent) that reflect immediate cargo values, and exchange‑traded futures that provide hedging and speculation tools. Traders, producers and refiners use these instruments to manage price risk.

Uses, distinctions and notable facts

- As a benchmark, Brent influences pricing for many non‑North Sea crudes that are priced as a differential to Brent.

- Differences from other benchmarks: compared with WTI, Brent is seaborne and more closely tied to international oil flows; WTI historically reflected inland U.S. supply and transport dynamics.

- Brent’s composition is periodically reviewed: the exact blend and delivery arrangements adapt to changes in North Sea production and logistics.

Because Brent functions as both a physical product and a financial reference, its price movements are watched by governments, companies and investors worldwide. Understanding its attributes—quality, origin, contract types and market role—helps explain why it remains central to global oil pricing.

Related articles

Author

AlegsaOnline.com Brent Crude Leandro Alegsa

URL: https://en.alegsaonline.com/art/13940

Sources

- onefinancialmarkets.com : "UK brent, crude oil, brent crude,"

- investing-for-beginner.org : "ベーシックな支払い方法について" · web.archive.org