Social Security (United States): Overview, Funding, Benefits, and History

Social Security (OASDI) is the U.S. federal program providing retirement, survivors, and disability insurance. It is funded mainly by payroll taxes and administered by the Social Security Administration.

Overview

In the United States, "Social Security" commonly refers to the federal Old-Age, Survivors, and Disability Insurance program, abbreviated OASDI. Administered by the Social Security Administration, the program provides income protection to eligible workers and their families through retirement benefits, survivor benefits for families of deceased workers, and disability benefits for workers who cannot continue gainful employment.

Image gallery

10 Images

Major components and benefits

Social Security benefits fall into three broad categories:

- Retirement insurance: Monthly benefits paid to eligible retirees. The earliest reduced retirement benefit can begin at age 62; the full retirement age depends on the worker's birth year and is typically between 66 and 67.

- Survivors insurance: Benefits for widow(er)s, dependent children, and sometimes parents when a worker dies.

- Disability insurance: Payments to insured workers who meet strict medical and work-history requirements and are unable to work.

How it is funded

Social Security is financed primarily through dedicated payroll taxes. Employees and employers each pay a share under the Federal Insurance Contributions Act (FICA); self-employed workers pay the equivalent under the Self-Employed Contributions Act (SECA). Payroll taxes are collected by the Internal Revenue Service and credited to two trust funds that support benefits. Earnings above an annually adjusted taxable maximum are not subject to the Social Security payroll tax; the cap changes each year (for example, in 2019 the cap was $132,900).

Eligibility and benefit calculation

Eligibility depends on a worker's earnings history and credited quarters of coverage. Benefits are calculated from a worker's lifetime earnings, indexed for wage growth, and converted into a Primary Insurance Amount that determines monthly payments. Cost-of-living adjustments (COLAs) can increase benefits periodically to help maintain purchasing power.

History and development

The modern Social Security system began with the Social Security Act of 1935, signed into law during the administration of President Franklin D. Roosevelt as part of the New Deal. Over subsequent decades the program expanded to include survivors and disability coverage and to refine benefit rules, eligibility, and administration. The program remains a central feature of the U.S. social safety net.

Challenges, reforms, and importance

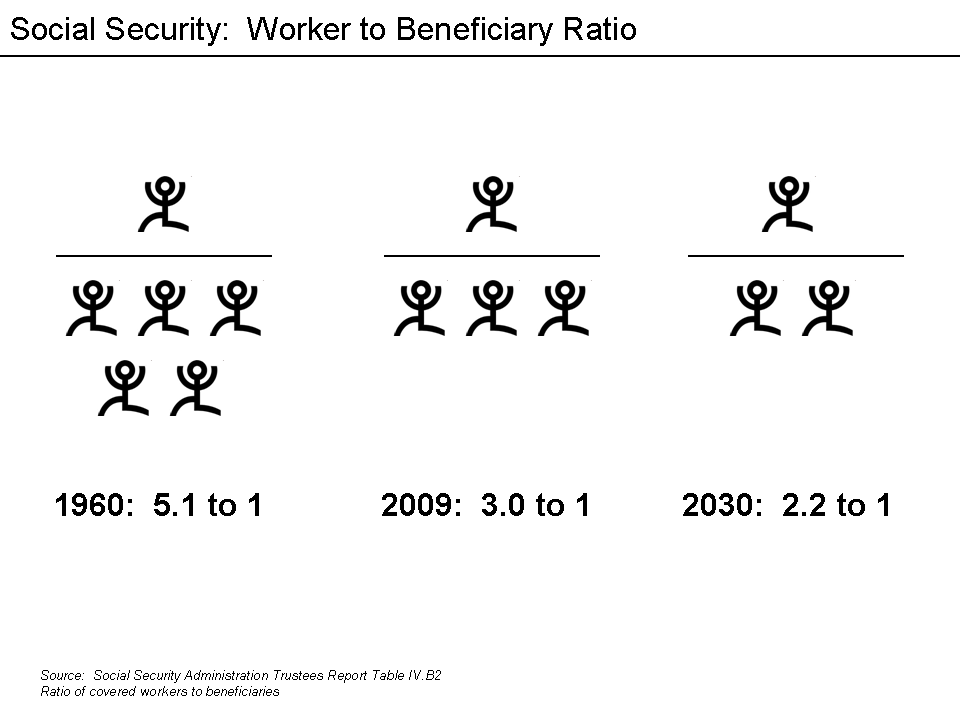

Social Security is a major source of income for many older Americans and for families of disabled or deceased workers. It faces long-term financing pressures driven by demographic trends—principally the aging population and changing worker-to-beneficiary ratios—which actuarial reports say could require policy changes to maintain full scheduled benefits over the long run. Debates about reform often focus on tax rates and caps, eligibility ages, benefit formulas, and measures to strengthen the trust funds.

Because of its size and social role, changes to Social Security have broad economic and political implications. For more background on program rules and history, see the Social Security Act discussions and technical descriptions of payroll taxes such as FICA/SECA.

Related articles

Author

AlegsaOnline.com Social Security (United States): Overview, Funding, Benefits, and History Leandro Alegsa

URL: https://en.alegsaonline.com/art/91446

Sources

- ssa.gov : Social Insurance Programs

- socialsecurity.gov : "Legislative History 1935 Social Security Act"

- access.gpo.gov : "US Code—Title 42—The Public Health and Welfare" · web.archive.org

- ssa.gov : "Contribution and Benefit Base"

- ssa.gov : A SUMMARY OF THE 2018 ANNUAL REPORTS

- ssa.gov : "Social Security & Medicare Tax Rates"

- college.hmco.com : "A Reader's Companion to American History: Poverty"