Monopolistic competition: definition, features, history, and examples

Monopolistic competition is a market structure with many sellers offering differentiated products. Firms have limited pricing power, nonprice competition is common, and free entry tends to eliminate long‑run profits.

Monopolistic competition is a common market structure in which many firms sell products that are similar but not identical. Unlike in perfect competition, individual sellers can influence the price of their own product because consumers perceive differences in quality, branding, location, or other attributes. At the same time, competition is far broader than in monopoly or oligopoly because many producers and buyers participate and entry into the market is relatively easy. For a concise formal context see related market forms.

Image gallery

2 Images

Key characteristics

- Many sellers and many buyers, each with a small share of the market.

- Product differentiation: goods or services are close substitutes but not perfect substitutes.

- Downward‑sloping demand for each firm: a single firm faces some ability to set price.

- Free entry and exit in the long run, which limits persistent economic profit.

- Nonprice competition such as advertising, packaging, and location strategies.

Because products are differentiated, each firm faces a demand curve that is more elastic than a monopolist’s demand but less elastic than that of an individual seller under perfect competition. Firms may obtain short‑run economic profits by emphasizing quality, unique features, or reputation, but these profits attract entry and tend to disappear over time. For a comparison with the idealized case where products are homogeneous see perfect competition.

Market behavior and welfare

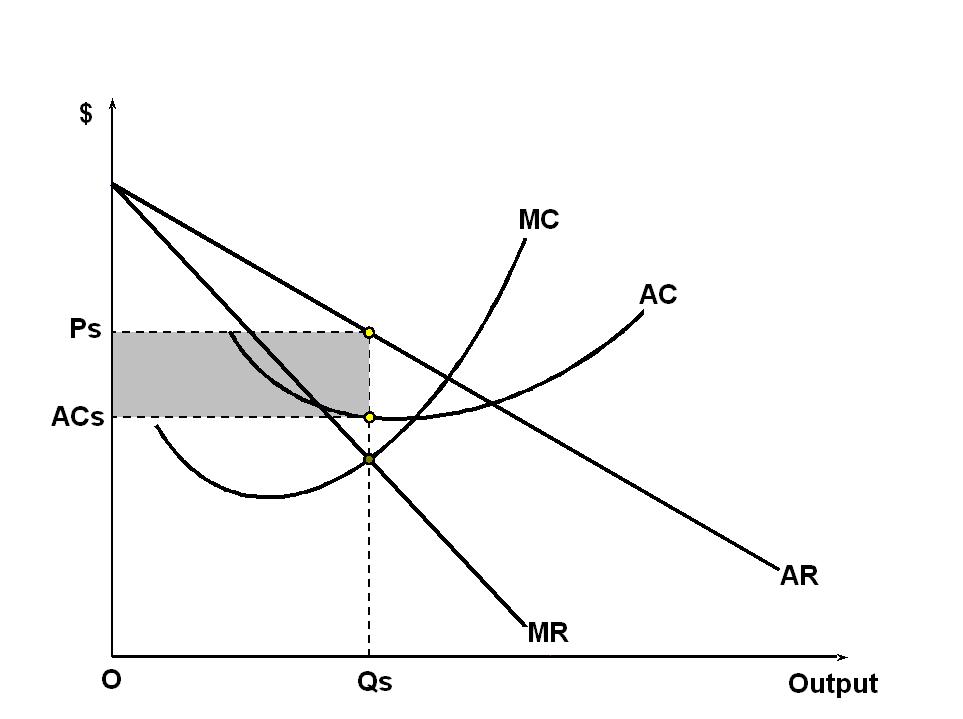

Firms in monopolistic competition typically price above marginal cost, producing less than the output that would minimize average cost. This outcome implies a degree of inefficiency—often called "excess capacity"—because firms do not operate at the lowest point on their average cost curves. On the other hand, the product variety and innovation that arise from differentiation can raise consumer satisfaction, so the net welfare effect depends on how consumers value variety versus the loss from markups.

Origins and theoretical development

The concept was developed in the early 20th century to bridge the gap between perfect competition and monopoly. Economists such as Edward Chamberlin and Joan Robinson articulated models in the 1930s showing how product differentiation and many sellers lead to distinctive equilibrium outcomes. Their work emphasized the role of advertising, branding, and product variety in shaping market structure and firm strategy.

Examples and practical importance

Many real‑world industries approximate monopolistic competition: retail stores, restaurants, clothing labels, local service providers, and personal care products. A simple illustration is a town’s bakeries: several bakeries serve overlapping customer bases, but one bakery can charge a small premium for a signature pastry, a convenient location, or a strong local reputation. The practical consequences include persistent marketing expenditures, emphasis on branding and convenience, and frequent product differentiation to maintain market share and customer loyalty. See a pricing and location example at local pricing example.

Distinctions and notable facts

- Monopolistic competition differs from oligopoly mainly in the number of firms: oligopolies have few dominant firms and strategic interaction is central.

- Unlike monopoly, long‑run economic profits are typically driven to zero by entry, though firms retain some price discretion.

- Policy concerns include the tradeoff between variety and efficiency, and how advertising affects consumer choices and information.

In summary, monopolistic competition captures an intermediate and frequently observed market form where diversity, modest pricing power, and dynamic entry shape outcomes for firms and consumers alike.

Related articles

Author

AlegsaOnline.com Monopolistic competition: definition, features, history, and examples Leandro Alegsa

URL: https://en.alegsaonline.com/art/66121