Everyday checking accounts: access, common features, fees, and regulation

Guide to everyday checking accounts: how to access funds, typical features like debit cards, ATMs, overdraft, fees and interest, and the key regulatory and deposit-insurance protections to compare.

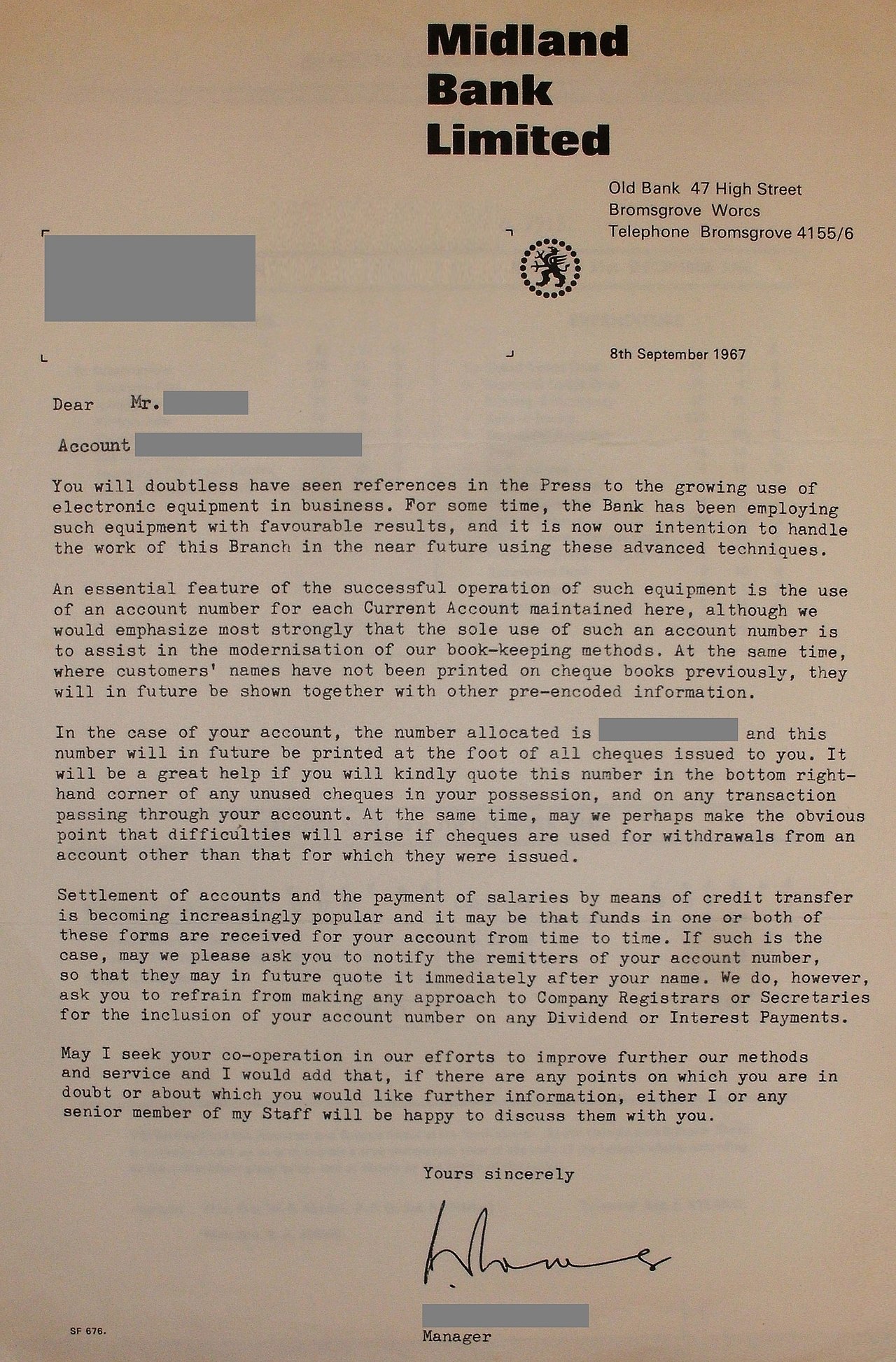

Overview

A checking account is a form of deposit account kept at a bank or credit union that is primarily intended for everyday payments and cash management. These accounts are designed for frequent use and provide ready access to funds for purchases, bill payments, and withdrawals.

Image gallery

2 Images

How account holders access funds

Account holders typically move money in and out of checking accounts using a variety of methods, such as:

- written or electronic checks;

- debit cards at point-of-sale terminals;

- automated teller machines (ATMs);

- online and mobile banking transfers, including direct deposit and automated clearing house (ACH) transactions;

- electronic debits and person-to-person payment services linked to the account.

Common features and costs

Checking accounts are meant to be highly liquid and support frequent deposits and withdrawals. Many providers charge monthly maintenance fees or per-transaction fees, though fee structures vary widely and some accounts waive charges if the customer meets certain conditions (for example, maintaining a minimum balance or setting up direct deposit).

Some checking accounts pay interest, but rates are generally lower than those on savings or other investment products. Overdraft protection is another common feature; it allows transactions that exceed the available balance to be covered for a fee or by linking to another account. Consumers should review terms carefully for fees, transaction limits, and overdraft policies.

Naming and regulation

In the United Kingdom and several other countries, the same product is often called a current account. Checking accounts are subject to banking regulations and deposit insurance in many jurisdictions—for example, in the United States eligible accounts at banks and many credit unions are insured by agencies such as the FDIC or NCUA—so the specific protections, rules, and consumer rights depend on local law and the institution.

Tags

Related articles

Author

AlegsaOnline.com Everyday checking accounts: access, common features, fees, and regulation Leandro Alegsa

URL: https://en.alegsaonline.com/art/19092