Tariff (customs duty): purpose, types, history and economic effects

A tariff is a tax on goods crossing borders. This article explains types of tariffs, their uses for revenue and protectionism, historical development, economic effects, and how they differ from other trade measures.

A tariff is a levy imposed on goods as they move between countries. Most commonly applied to imports, tariffs raise the price of foreign products to domestic buyers and can also be applied to exports in some jurisdictions. Governments use tariffs for several reasons: to generate revenue, to protect nascent or strategic domestic industries, to pursue policy goals such as environmental or health protection, or to exert leverage in trade negotiations. For a concise definition and legal context see tariff overview.

Image gallery

7 Images

Common forms and mechanics

Tariffs take several technical forms. An ad valorem tariff is charged as a percentage of the goods' value; a specific tariff is a fixed amount per unit (for example, per kilogram or per item); and compound tariffs combine both approaches. Tariffs are typically administered at customs when goods are imported (imports) but export duties (exports) are also used by some states. Preferential rates, exemptions, and tariff schedules for particular product categories are common features of modern tariff regimes.

History and policy rationale

Historically, tariffs were a principal source of government revenue before the rise of broad-based income and consumption taxes. They were central to mercantilist policies that emphasized accumulating wealth through trade surpluses. In later centuries, tariffs became instruments of industrial policy and protectionism, intended to give local firms time to develop. Governments also cite revenue needs and public policy objectives—such as protecting public health or natural resources—as reasons for maintaining duties. For the revenue perspective, see government revenue purposes; for protectionist policy considerations, see protectionism.

Economic effects and examples

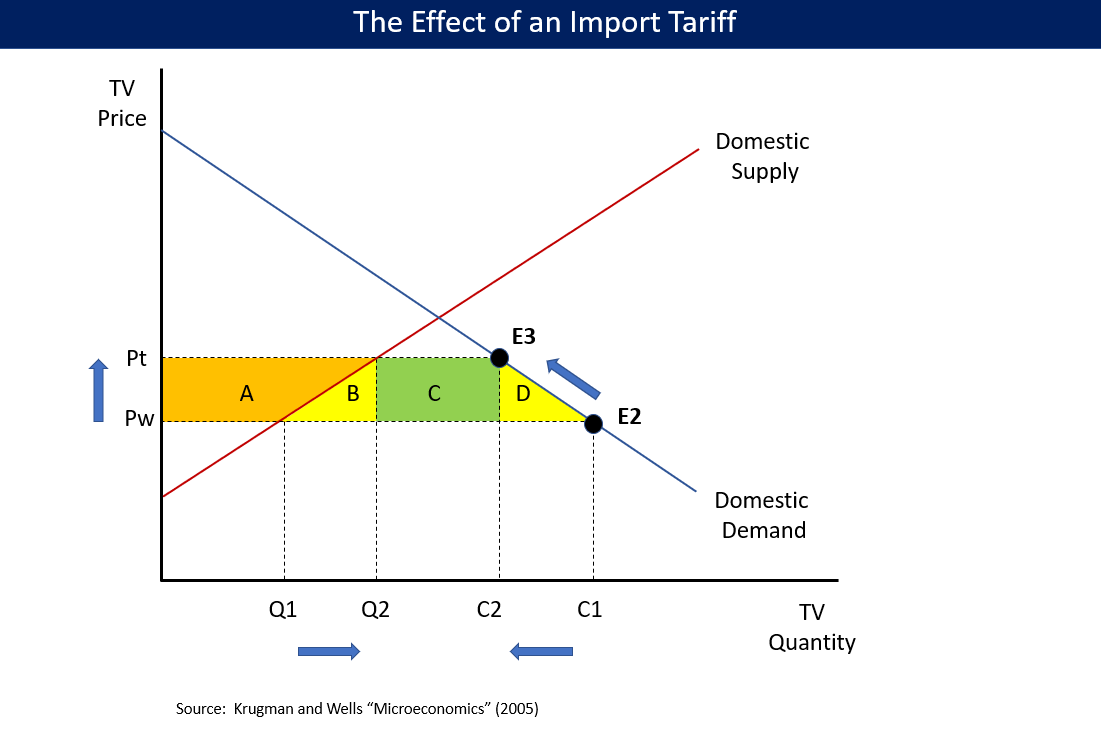

Tariffs raise the domestic price of imported goods, which benefits protected producers but tends to increase costs for consumers and downstream industries that use imported inputs. They can reduce import volumes, distort comparative advantage, and invite retaliatory measures from trading partners. At the same time, tariffs can be used temporarily in response to sudden import surges or market disruption. In practice, tariffs often coexist with non-tariff measures—such as quotas, standards, and licensing—that influence trade flows.

Distinctions and notable facts

- Tariffs differ from internal taxes (like sales taxes or value-added taxes) because they are specifically levied at a border on cross-border transactions.

- International rules and bilateral or regional free trade agreements commonly aim to reduce tariffs between signatories; such agreements are a pathway toward tariff elimination.

- Non-tariff barriers and sanitary or phytosanitary regulations can act as substitutes for tariffs in restricting trade.

- Tariff systems often include classifications and schedules that determine precise rates for specific goods; administration requires customs valuation and enforcement.

Understanding tariffs requires attention to both their technical design and their broader economic and political context. For introductory materials and policy debates consult general resources and trade institutions via further reading or policy portals at imports guidance and exports guidance, and summaries of fiscal use at revenue policy and trade policy rationales at protectionist measures.

History

Customs duties have existed for a very long time; as early as antiquity and the Middle Ages, they were mostly levied in the form of concurrence duties - comparable to a toll - with the emperor losing more and more sovereign rights to territorial lords (and thus the individual cities). In the age of mercantilism, tariffs were used specifically as an economic policy measure to protect the balance of payments and domestic producers. Prohibitive tariffs were intended to prevent the import of foreign products in the first place, educational tariffs to promote the development of domestic industry, and protective tariffs to protect it from (cheaper-producing) foreign competitors.

Since 1947, tariffs have been significantly reduced worldwide under the GATT. Since 1995, this has been done within the framework of the World Trade Organization.

Import, transit and export duty

General

A distinction is made between import (or import), transit (or transit) and export (or export) duties, depending on the movement of the goods on which a duty is levied. In most cases, the term customs duty refers to an import duty. These customs duties have become the most important. Through them, a state gains foreign currency (financial customs duty) or can protect domestic economic enterprises from foreign competition (protective customs duty).

According to Art. II GATT, Member States are obliged to set maximum tariffs (so-called contract duties) which will not be exceeded. Each Member State has established this in the form of a list indicating the maximum tariffs for certain products.

Transit duties are inadmissible under Art. V:3 GATT inadmissible. In order to facilitate transit traffic, trucks which only pass through a country without exporting anything to that country bear the TIR marking and are sealed. This does not apply to intermediate or raw products which are brought into an economic area, processed there and then re-imported into the original economic area (processing traffic).

Export duties are rarely imposed because it is usually in a country's interest to sell goods to foreign countries and thereby generate revenue. Export duties make the export of goods more expensive and thus reduce it. Especially for developing countries, however, there are reasons to impose export duties:

- they give the State a share of the revenue (fiscal reasons) if the exported product can be sold on the world market despite being subject to customs duties (e.g. rare raw materials),

- they prevent urgently needed scarce goods (shortages) from being exported instead of being sold on the domestic market (e.g. food),

- they can defuse trade disputes and possibly avert the imposition of import duties by another country (e.g. textiles).

The opposite of export duties are export subsidies.

Collection of import duties in Germany

Customs duties are collected by the customs authorities of a country. Customs offices are located at the central hubs of goods traffic. Most of these customs offices are stationary, e.g. in ports, airports, railway stations or border crossings. In addition, the customs administration is also active on a mobile basis through the KEV and KEG (control units traffic and control units border area), for example on motorways and interurban roads.

The import procedure is divided into the following steps:

- Bringing the goods into the country (in doing so, the customs road constraint must be observed)

- Presentation of the goods

- Entry summary declaration (ESumA) of the goods

- Customs declaration

- Examination and acceptance of the customs declaration

- possibly inspection of the goods (target: 5 percent of the goods)

- payment of import duties (customs duties, import turnover tax, excise duties, etc.)

- surrender of the goods

Goods that are found to be dutiable or that cannot be conclusively assessed are taken into custody by Customs. The consignee or an authorised representative must provide the customs with requested documents and, if necessary, make the customs payment in order to have goods handed over.

An authorized agent can be, for example, Deutsche Post (assuming the corresponding order from the recipient/sender).

If no authorised representative is specified, customs handling is to be carried out by the consignee, which is known as self-clearance. Goods delivered by post may be labelled "self-customs" by customs and must then be handed in by the shipping company at the nearest customs office to the recipient's location. The consignee must then be informed by the "Notification of Receipt of a Consignment of Third Country Goods" (green card) by the shipping company. The consignee must then provide the information/documents specified in "Notice of Customs Handling of a Mail Item".

In Germany and the EU, customs clearance is possible at internal customs offices, whereas Switzerland only has customs clearance at the border, i.e. all goods traffic must undergo customs clearance at the border.

Related articles

Author

AlegsaOnline.com Tariff (customs duty): purpose, types, history and economic effects Leandro Alegsa

URL: https://en.alegsaonline.com/art/96397

Sources

- en.wikisource.org : "Tariff"