Elasticity (economics): measuring responsiveness of supply, demand and income

Elasticity quantifies how one economic variable responds to changes in another—most often price or income. Explains types, measurement, determinants, examples, history and policy relevance.

Elasticity is a central concept in economics that describes how much one variable changes in response to a change in another. Most commonly analysts measure how quantity demanded or supplied responds to a change in price or to changes in income. Elasticity is a unit‑free ratio of percentage changes, which makes it useful for comparing responsiveness across different markets, goods and time periods.

Image gallery

10 Images

Common types

- Price elasticity of demand — the percentage change in quantity demanded divided by the percentage change in price. It is usually negative because demand falls when price rises; analysts often report its absolute value.

- Price elasticity of supply — the percentage change in quantity supplied divided by the percentage change in price. Supply elasticities are typically positive. See also supply.

- Income elasticity of demand — how quantity demanded responds to changes in income. Positive values indicate normal goods; negative values indicate inferior goods.

- Cross‑price elasticity — the response of demand for one good to a price change of another good; positive for substitutes and negative for complements (related to demand interactions).

Measurement and interpretation

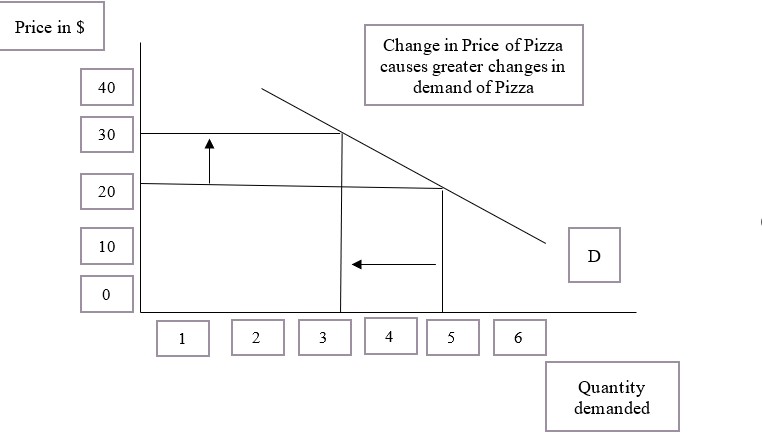

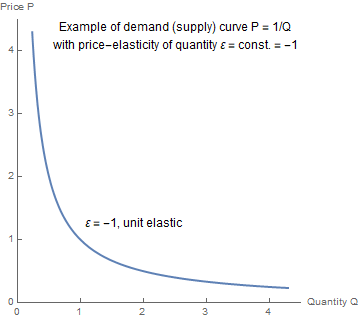

Elasticity is calculated as the ratio of percentage changes. A simple formula for price elasticity of demand is: elasticity = (% change in quantity) / (% change in price). For small changes, the point elasticity uses calculus: e = (dQ/dP) × (P/Q). For larger discrete changes analysts often use the midpoint (arc) formula to avoid asymmetry. Example: if price rises by 2% and quantity demanded falls by 1%, the price elasticity of demand = −1% / 2% = −0.5 (often reported as 0.5 in absolute terms). Values below 1 in absolute value imply inelastic demand; values above 1 imply elastic demand.

Determinants of elasticity

- Availability of substitutes: more close substitutes → more elastic demand.

- Necessity versus luxury: necessities tend to be inelastic; luxuries more elastic.

- Proportion of income: goods that take a larger share of income tend to have more elastic demand.

- Time horizon: demand and supply usually become more elastic over longer time periods as consumers and producers adjust.

- Market definition: narrowly defined markets (e.g., a specific brand) are more elastic than broad categories.

History, uses and policy relevance

The term "elasticity of demand" was popularized by late 19th‑century economists such as Alfred Marshall to formalize responsiveness in market analysis. Today elasticity informs business pricing, government tax policy and welfare analysis: for example, the effect of a tax on quantity sold and tax incidence depends critically on elasticities of supply and demand. Elasticities also guide revenue forecasts—raising price can increase total revenue when demand is inelastic, but reduce revenue when demand is elastic.

Examples and notable facts

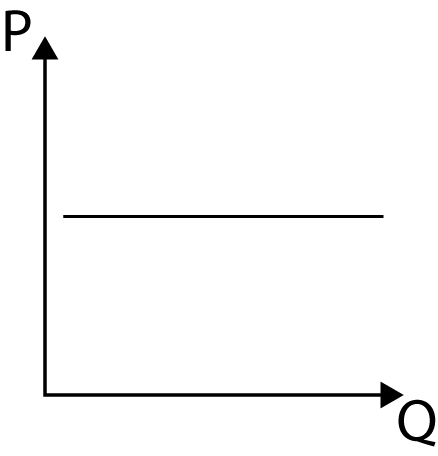

Practical examples help to illustrate the concept. If consumers cut purchases of DVDs substantially when their prices rise, DVDs have elastic demand. By contrast, a good like salt often shows very inelastic demand: price changes have little effect on quantity consumed because it is a small expenditure and a basic necessity. Perfectly elastic demand (a horizontal response) and perfectly inelastic demand (a vertical response) are theoretical extremes; most real markets lie between these cases.

Accurate measurement requires reliable data and attention to method: short‑run estimates differ from long‑run ones, and cross‑sectional comparisons require similar definitions and time frames. Policymakers and firms use elasticity to predict behavioral responses and to design interventions that account for how strongly people or producers will react to price, income or related goods' price changes.

For further reading on related concepts see discussions of supply, demand, taxation effects and welfare analysis in standard texts or online resources referenced by economic institutions: overview materials often present graphical, algebraic and empirical approaches to elasticity.

Motivation

The motivation for using elasticities stems from the fact that the absolute change in the dependent variable provides insufficient information about the structure of a response.

For example, consider a product whose price is increased by €1, whereupon sales fall by 10,000 units. The absolute values reveal little about the scope of the change in demand. The benchmark is missing: Was the price at the starting point €10 or €100? Did sales drop from 50,000 to 40,000 or from 1,000,000 to 990,000? In contrast, a useful measure of the impact of an instrument is elasticity, which assumes relative changes. Since elasticity does not contain a dimension (such as "€" or "units"), it enables the comparability of similar values.

Mathematical representation

An independent variable

To grasp this verbal definition mathematically, consider a function  .

.

Analogous to the concept of the difference quotient as a lead-in to the differential quotient, the so-called arc elasticity (also called distance elasticity) is first assumed. Consider a finitely small change Δ in  the variable

the variable  and Δ

and Δ  the variable

the variable  , resulting in the relative changes Δ

, resulting in the relative changes Δ  and Δ

and Δ  . The average relative change of respect to a relative change of gives the arc elasticity

. The average relative change of respect to a relative change of gives the arc elasticity

an. Letting Δ  go, one obtains as an infinitesimal notion the elasticity function of with respect to all , for which is

go, one obtains as an infinitesimal notion the elasticity function of with respect to all , for which is  differentiable and not a

differentiable and not a  zero,

zero,

,

which also

can be written. This elasticity is also called point elasticity.

It can also be shown that elasticity can also be represented as

.

.

Multiple independent variables

Consider a function  , which

, which  depends on one or more influence variables An elasticity ε

depends on one or more influence variables An elasticity ε  specifies the relative amount Δ

specifies the relative amount Δ  by which, ceteris paribus, the function value changes when an influence quantity changes by the relative amount Δ .

by which, ceteris paribus, the function value changes when an influence quantity changes by the relative amount Δ .  This results in the following for the arc elasticity

This results in the following for the arc elasticity

and with infinitesimal consideration

,

,

where ∂  denotes a partial derivative. Following this, this case with multiple independent variables is also called partial elasticity.

denotes a partial derivative. Following this, this case with multiple independent variables is also called partial elasticity.

Related articles

Author

AlegsaOnline.com Elasticity (economics): measuring responsiveness of supply, demand and income Leandro Alegsa

URL: https://en.alegsaonline.com/art/30605