Cheque (Check): A Practical Guide to the Paper Payment Instrument

A cheque (check) is a written order directing a bank to pay a specific sum from the drawer’s account to a named payee. This article explains parts, types, history, use, and modern relevance.

Overview

A cheque (spelled "check" in American English) is a negotiable paper instrument that orders a bank to pay a stated amount of money from the account of the person or organisation that wrote it (the drawer) to a named recipient (the payee) or to bearer. Traditionally presented at a bank counter or deposited into an account, cheques serve as an alternative to cash and electronic transfers. While their use has declined with the rise of electronic payments, cheques remain important for certain transactions, record-keeping, and in jurisdictions where digital access is limited.

Image gallery

10 Images

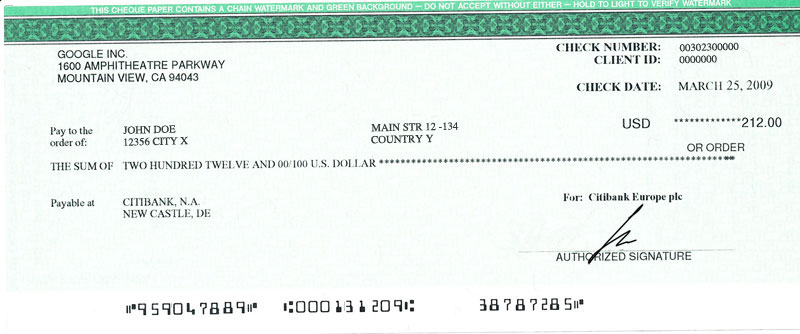

Key parts and common types

- Drawer: the person or entity who writes and signs the cheque.

- Drawee: the bank directed to pay the amount.

- Payee: the person or business named to receive payment.

- Payee line, date, amount: the fields that specify who receives the funds, when, and how much.

- Endorsement: the payee’s signature on the back used to transfer or deposit the cheque.

- Order cheques: payable only to the named payee.

- Bearer cheques: payable to whoever holds the cheque.

- Crossed cheques: marked to restrict payment to a bank account rather than cash.

- Post‑dated and stale cheques: dated for future payment or too old to be presented, respectively.

How a cheque is processed

The typical lifecycle begins when the drawer issues a cheque to a payee. The payee deposits or presents it to their bank, which acts as a collecting bank and forwards the cheque to the drawer’s bank (the drawee) through clearing channels. The drawee verifies the signature and availability of funds; if approved, it debits the drawer’s account and credits the payee’s bank. Modern systems often use cheque truncation or image exchange so that physical movement of paper is minimised. A cheque can be endorsed to transfer rights, and some cheques can be certified or guaranteed by a bank to assure payment.

History and development

In various forms, written payment orders have existed for many centuries, evolving from early bills of exchange and account transfers used by merchants. Cheques as we recognise them grew with modern banking systems in the 18th and 19th centuries and became widely used in the 20th century for non‑cash payments. Technological advances — magnetic ink character recognition (MICR), automated clearing houses, and digital imaging — reshaped cheque handling in the late 20th and early 21st centuries. In recent decades, cheque volumes have fallen as electronic transfers, card payments, and mobile banking gained prominence.

Uses, advantages, and limitations

Cheques are useful where a paper record is preferred, for payments that require signatures, or when parties do not share compatible electronic systems. They can be post‑dated to schedule payments and, when crossed or account‑to‑account deposited, reduce the risk of immediate cashing by an unintended bearer. However, cheques can be slower to clear than electronic transfers, are susceptible to forgery and alteration if poorly secured, and may incur processing fees. Many jurisdictions impose rules on presentation periods and liability for bounced or dishonoured cheques.

Practical considerations and notable facts

Financial institutions often provide cheque books and set guidelines for safe use: write the amount in both numerals and words, avoid leaving blank spaces that can be altered, and keep cheques secure. A cheque made out without an amount or left unsigned can be dangerous: an unsigned or blank cheque is essentially a promise with missing terms and can be misused. For more on banking services and account matters see financial institutions. To understand local clearing and deposit procedures consult your bank or clearing authority via clearing information. For risks associated with open or blank instruments, read guidance on what constitutes a blank cheque.

Questions and answers

Q: What is a cheque?

A: A cheque is a paper used to give money from one person or business to another person or business.

Q: What does a cheque do for the person getting it?

A: A cheque allows the person getting it to go to a bank and get money.

Q: What does a cheque represent for the person writing it?

A: A cheque represents a promise to pay the bank that is giving the money to the person who turned the cheque in.

Q: Who should be written on a cheque?

A: A cheque should be written to a person or business.

Q: Why is writing a cheque with no recipient a bad idea?

A: Writing a cheque with no recipient can be very bad because if it is lost, anyone who finds it can get the money.

Q: What is a blank cheque?

A: A cheque that is written to a person but does not have the amount of money written is a blank cheque.

Q: How long have cheques been in use?

A: Cheques have been used for over a thousand years, but they became popular in the 20th century for paying money without using cash.

Author

AlegsaOnline.com Cheque (Check): A Practical Guide to the Paper Payment Instrument Leandro Alegsa

URL: https://en.alegsaonline.com/art/19250